Freetech Road Recycling Technology (Holdings) Limited (HKG:6888) shareholders would be excited to see that the share price has had a great month, posting a 26% gain and recovering from prior weakness. Longer-term shareholders would be thankful for the recovery in the share price since it’s now virtually flat for the year after the recent bounce.

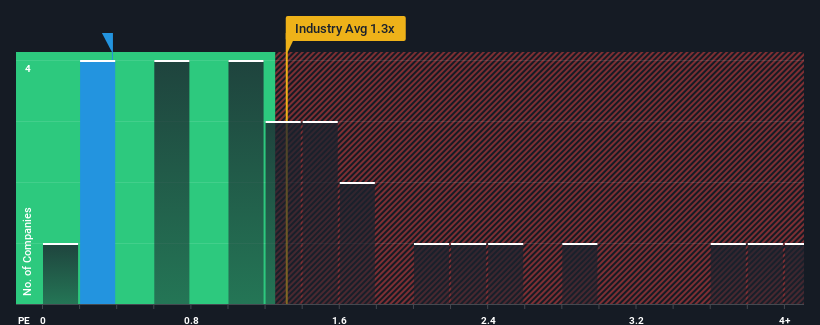

In spite of the firm bounce in price, considering around half the companies operating in Hong Kong’s Infrastructure industry have price-to-sales ratios (or “P/S”) above 1.3x, you may still consider Freetech Road Recycling Technology (Holdings) as an solid investment opportunity with its 0.4x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it’s justified.

See our latest analysis for Freetech Road Recycling Technology (Holdings)

What Does Freetech Road Recycling Technology (Holdings)’s Recent Performance Look Like?

Revenue has risen firmly for Freetech Road Recycling Technology (Holdings) recently, which is pleasing to see. It might be that many expect the respectable revenue performance to degrade substantially, which has repressed the P/S. If that doesn’t eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

Although there are no analyst estimates available for Freetech Road Recycling Technology (Holdings), take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Freetech Road Recycling Technology (Holdings) would need to produce sluggish growth that’s trailing the industry.

Retrospectively, the last year delivered a decent 14% gain to the company’s revenues. Still, revenue has barely risen at all in aggregate from three years ago, which is not ideal. Therefore, it’s fair to say that revenue growth has been inconsistent recently for the company.

Comparing that to the industry, which is predicted to deliver 7.5% growth in the next 12 months, the company’s momentum is weaker, based on recent medium-term annualised revenue results.

With this in consideration, it’s easy to understand why Freetech Road Recycling Technology (Holdings)’s P/S falls short of the mark set by its industry peers. Apparently many shareholders weren’t comfortable holding on to something they believe will continue to trail the wider industry.

What Does Freetech Road Recycling Technology (Holdings)’s P/S Mean For Investors?

Despite Freetech Road Recycling Technology (Holdings)’s share price climbing recently, its P/S still lags most other companies. Typically, we’d caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Freetech Road Recycling Technology (Holdings) revealed its three-year revenue trends are contributing to its low P/S, given they look worse than current industry expectations. At this stage investors feel the potential for an improvement in revenue isn’t great enough to justify a higher P/S ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

It is also worth noting that we have found 3 warning signs for Freetech Road Recycling Technology (Holdings) (1 is concerning!) that you need to take into consideration.

If you’re unsure about the strength of Freetech Road Recycling Technology (Holdings)’s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we’re helping make it simple.

Find out whether Freetech Road Recycling Technology (Holdings) is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.